Market Recap – Week Ending Jan. 19

S&P 500 Hits New High; Key GDP, PCE Reports This Week

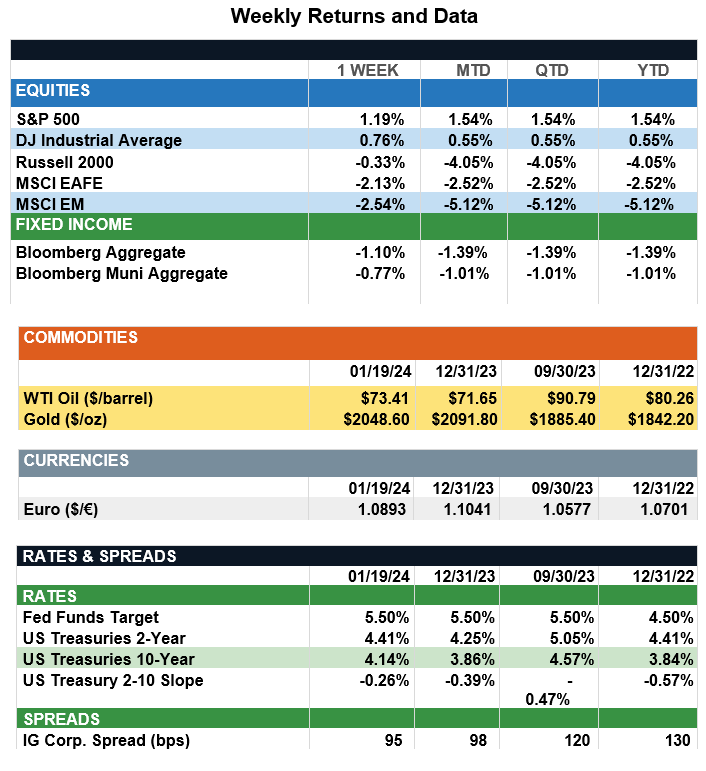

Overview: Stocks were mixed across the world last week. In the U.S., the S&P 500 index reached a new all-time high, ending the week 1.2% higher on the heels of strong retails sales which beat expectations and supported the resilience of consumer spending. On the international front, both developed markets (MSCI EAFE) and emerging markets (MSCI EM) were weaker, down 2.1% and 2.4%, respectively. Markets are dealing with continued conflict in the Middle East, overall increased geopolitical risk, and above-consensus consumer price (CPI) reports in the Euro that have elevated investor fears inflation may be more difficult to bring down than expected. In bonds, yields rose to their highest levels of the year as market expectations the Federal Reserve will begin to cut rates at their March 20 meeting decreased. Futures markets now are pricing in about a 50/50 chance of a 0.25% rate cut in March, down from about a 75% probability just a week ago. The 2-Year and 10-Year Treasury yields ended last week higher at 4.41% and 4.14%, respectively, with the 10-year Treasury higher by 28 basis points since the beginning of 2024. As the markets look for clues to future Fed direction, two important economic numbers will be closely watched this week. The first is Thursday’s release of 2023 fourth-quarter gross domestic product (GDP), expected to report at 2.0%. On Friday, personal consumption expenditures (PCE) will be reported, which includes the Fed’s preferred measure of inflation, the core PCE Price Index. Core PCE is expected to decrease on an annualized basis from to 3.0% in December from 3.2% the prior month, as the Fed continued their policies to reduce inflation to their long-term target of 2%.

Update on Earnings (from JP Morgan): With 10% of market cap having reported, fourth-quarter S&P 500 operating earnings per share (EPS) is tracking +4.1% y/y growth. However, similar to 3Q23, we continue to see divergence between the operating earnings estimates and pro-forma estimates, which currently are tracking a y/y decline of 2.2%. As a brief reminder, while operating earnings are unadjusted and a better indicator of “economic profit,” the market prices off pro-forma earnings, which are therefore more useful in explaining recent market moves. So far, results have been heavily impacted by the financial sector. Overall, the sector is tracking a pro-forma earnings contraction of 25%, primarily due to results in the banking industry. Among the banks, earnings have been hampered by a slew of FDIC charges related to the banking crisis we saw earlier in 2023. Separately, net interest income continues to decline, as loan growth stalls and deposits reprice higher. Provisions for loan losses have ticked up yet again due to weakening credit quality and increasing net charge-offs. These headwinds have been partially offset by a slight recovery in investment banking activity and strong trading revenues. Excluding financials, results have come in above expectations, with an earnings surprise of +5% versus an earnings surprise of -21% including financials. In the consumer sectors, for instance, results from the early reporters have been marked by the successful clearing of bloated inventories, cost management, resilient pricing power and margin expansion. Elsewhere, the tech sectors seem set for another strong quarter, as continued head count and cost management along with the strong demand for digital and AI-related capabilities support software earnings growth. Looking ahead, the next two weeks will be key for results as the index’s largest names will report earnings and provide guidance on expectations for profits in 2024.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.