Market Recap – Week Ending Jan. 5

Global Stocks Lower; Key Data, Earnings Reports Due This Week

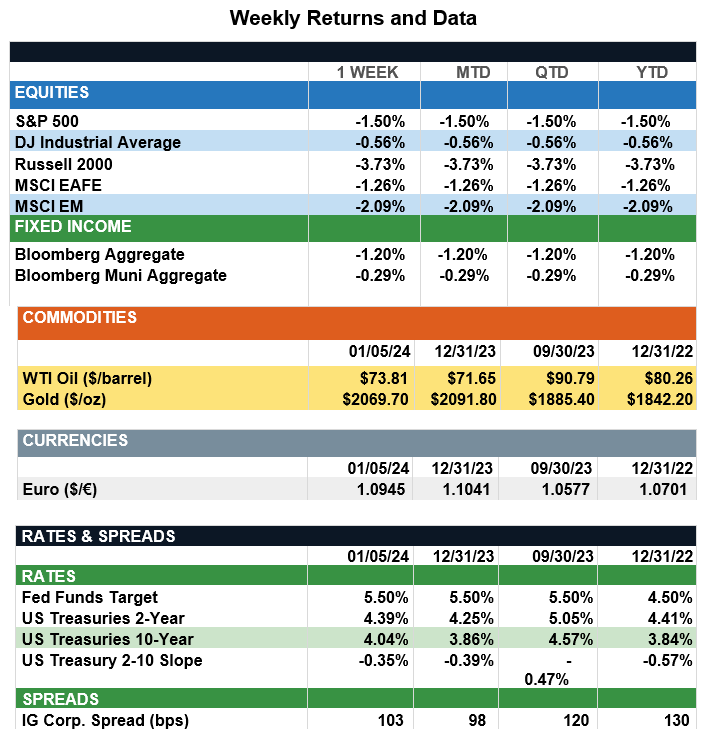

Overview: Stocks across the globe began 2024 lower as markets continue to evaluate Federal Reserve policy to assess the future path of interest rates and the ensuing effect on economic conditions. In the U.S., the S&P 500 index finished the week lower by 1.5%. Stronger than expected job growth, along with minutes from the last Fed meeting, added uncertainty to the timing and magnitude of any interest rate cuts for 2024. In fact, the minutes from the last meeting “reaffirmed that it would be appropriate for policy to remain at a restrictive stance for some time until inflation was clearly moving down sustainably toward the Committee’s objective.” Bond yields rose on the week, with the 2-year and 10-year Treasury notes finishing the week at 4.39% and 4.04%, respectively, leading to negative returns in both taxable and municipal bonds to begin the year. This week, investors will look for clues on inflation from the December Consumer Price Index (CPI) and from producer prices (PPI) due out on Thursday and Friday, respectively. On Thursday, core CPI is expected to fall from 4.0% to 3.8% in December on a year-over-year basis, as the Fed continues to bring inflation down to their 2% target. Other key data will come in the form of earnings, as the latest earnings season will kick off Friday with results from big banks such as Bank of America, Citigroup, JPMorgan Chase and Wells Fargo. Other key earnings reports will come that day from UnitedHealthcare, Delata, and Blackrock as the fourth-quarter 2023 earnings season gears up.

Update on the Dollar (from JP Morgan): After moving sideways during the first half of 2023, the dollar continued its decline to end 2% down in 2023 (now -11% from its October 2022 peak). In fact, it depreciated against almost every major DM currency except the Japanese yen. After more than 10 years of dollar strength, could this be the start of a new cycle? History suggests the dollar tends to move in multi-year cycles, with long periods of weakness following extended periods of strength. Dollar movements are driven by interest rate and growth differentials and sentiment in the short term, but by current account balances over the long term. There are many factors that could put downward pressure on the dollar in 2024 and beyond. The Fed is likely to cut first out of the DM central banks, whereas others are expected to stay on pause for longer or even raise rates. In addition, with the end of negative interest rates in Europe and most likely Japan, interest rate differentials between the U.S. and other DMs will likely not be as wide as they were in the post-GFC period. Regarding growth, consumer spending, the bedrock of the U.S. economy, is set to slow after hitting what was likely a high-water mark in 3Q. Over the long term, the increasing current account deficit and federal debt also suggest further USD depreciation. At the same time, elevated geopolitical risks and any upward surprises in inflation could interrupt its path downward. For investors, a weaker dollar increases the opportunity for international equities and internationally exposed U.S. companies to perform well. Even after a year of strong U.S. outperformance, investors should avoid recency bias by ensuring their equity portfolios are properly diversified across different regions.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.