Market Recap – Week Ending Feb. 16

Stocks Mixed; Fed Meeting Minutes, Key Earnings This Week

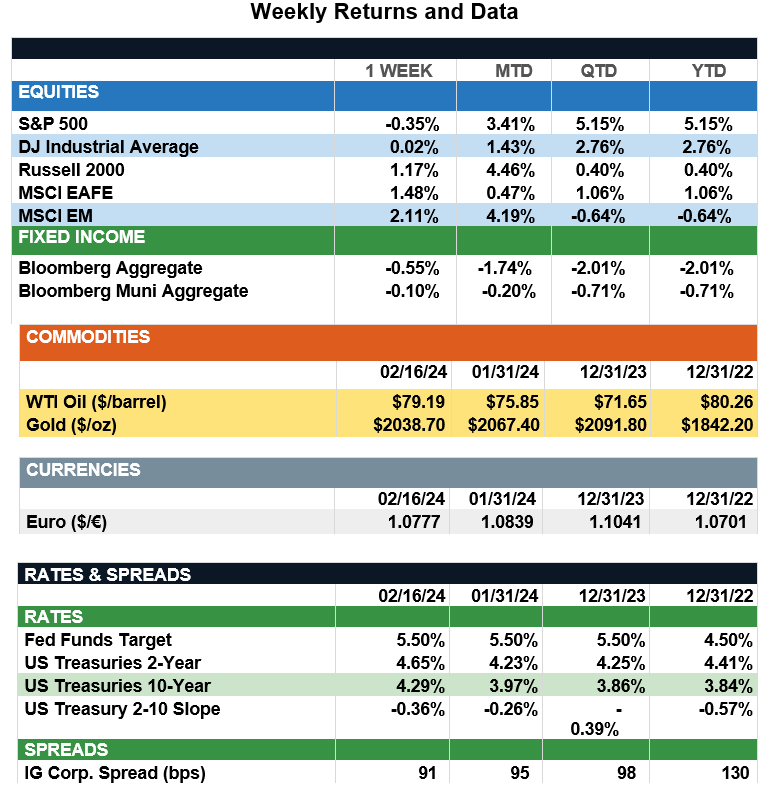

Overview: Stocks were mixed across the globe last week, as emerging markets (MSCI EM) and international developed (MSCI EAFE) posted positive returns of 2.1% and 1.5%, respectively. In the U.S., the S&P 500 index suffered its worst one-day drop in more than a year on Tuesday but recovered to finish the week lower by just 0.4%. The catalyst for Tuesday’s drop in the markets was the consumer price (CPI) report, where the headline inflation reading came in at 3.1% on an annualized basis, higher than the consensus of 2.9%. In addition, Friday’s producer price (PPI) report also showed an uptick in wholesale prices with PPI increasing by the highest amount in five months to 0.3% from the prior month, versus the expectation for a 0.1% increase. In the fixed income markets, yields increased as investors continue to assess the direction of the economy and the timing of rate cuts by the Federal Reserve. The 2-year and 10-year Treasury notes finished the week at 4.65% and 4.29%, respectively, and both notes are now about 40 basis points (0.40%) higher since the start of the year. In this holiday-shortened week, focus will be on the release of the minutes from the last Fed meeting on Wednesday. On the earnings front, key reports will come from Walmart and Home Depot on Tuesday, and tech giant Nvidia on Wednesday, as investors evaluate earnings and forward guidance for clues to the health of the consumer.

Update on Inflation and Wage Growth (from JP Morgan): Last week’s January CPI report came in above expectations with headline CPI rising 0.3% m/m and 3.1% y/y. Shelter prices, which increased 0.6% in January, accounted for more than two-thirds of the monthly increase in headline CPI. Excluding food and energy (core), CPI increased 0.4% m/m and 3.9% y/y, with the core services categories driving much of the increase. The core services index, which includes shelter, medical care services and transportation services, increased 0.7% m/m – a notable acceleration from a monthly gain of 0.4% in December. Despite the increase in overall CPI, there were continued signs of cooling in core goods, where prices fell 0.3% in January. While the January CPI report was hotter than expected, a healthy labor market has driven wage growth and in turn kept real wages, which is defined as nominal wages less inflation, positive. Since the start of 2023, the growth in average hourly earnings for private employees has outpaced the growth in headline CPI. Looking ahead, we expect this favorable dynamic to continue due to the resilient nature of the labor market and the broader cooling in inflation and therefore support consumption. Despite the monthly accelerations in headline and core CPI growth, the y/y headline CPI rate moderated to 3.1% versus 3.4% last January, with the core CPI rate staying unchanged. As such, we maintain our view the Federal Reserve will begin lowering rates in June, with additional economic data in the coming months to reiterate the broader disinflation we have seen over the last 12 months.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.