Market Recap – Week Ending Feb. 23

Strong Technology Earnings Push Stocks Higher

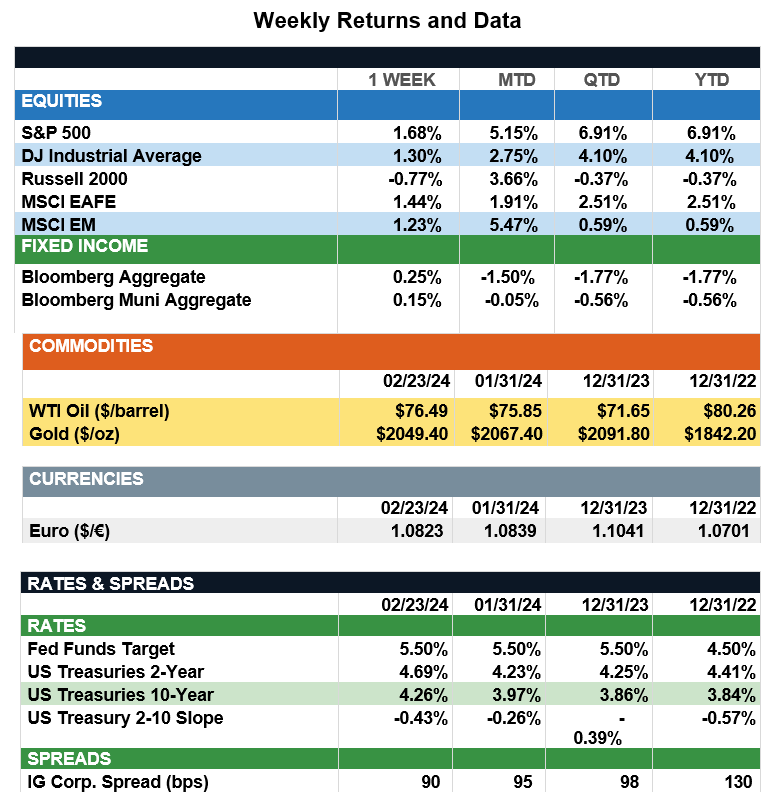

Overview: Stocks were higher around the world last week, as strong earnings in the technology sector helped the S&P 500 index to its best day in a year on Thursday. In the U.S., the S&P 500 finished the week higher by 1.7%, while international developed (MSCI EAFE) and emerging markets (MSCI EM) notched similar gains of 1.4% and 1.2%, respectively. In the bond markets, interest rates were relatively stable, with the 2-year and 10-year Treasury notes finishing the week at yields of 4.69% and 4.26%, respectively. Minutes from the January Federal Open Market Committee (FOMC) meeting showed Fed members remain sensitive to inflationary risks and expressed a tone of patience in delivering future rate cuts. The minutes acknowledged major inflation progress, yet cautioned the current strength of economic activity may delay rate cuts, which are now expected by market participants to begin around the June Federal Reserve meeting (see commentary below). In economic data, manufacturing data (PMI) showed strength, rising to a 17-month high in January while the services PMI remained in expansionary territory. Meanwhile, existing home sales increased in January on the back of lower mortgage interest rates. As the next section outlines, market expectations for Fed policy will be highly dependent on economic reports that give insight into the health of consumer spending and economic growth.

Update on Federal Reserve Policy (from JP Morgan): Market expectations for Fed policy have swung dramatically over the past few months, from the higher-for-longer narrative to expectations of aggressive policy easing. With stronger-than-expected jobs and growth data this year, and inflation still mild, investors have had to reassess their outlook for policy rates. The past five months have been a wild ride for policy expectations. In October, investors expected minimal change in interest rates in 2024. Sentiment then shifted dramatically after the Fed’s dovish pivot in December, sparking optimism for swifter policy easing this year. Soon after, markets turned increasingly dovish, calling for a rate cut by March and ~170bps of easing, more than double the Fed’s December forecast. Today, markets are pricing in a 79% probability of a rate cut by June and a total of 82bps of cuts for the year, suggesting at least three cuts with a chance of a fourth. Bond and equity markets have responded differently to these shifts. Bond markets repriced in line with policy expectations, with the 10Y Treasury yield rising from 3.88% to 4.26% this year. As the Fed prepares to cut rates, current bond yields offer investors an attractive entry point to add duration and income. For equities, prices have continued moving higher with the S&P 500 up 21.9% since October and 6.9% year-to-date. So long as higher yields are being driven by expectations for stronger growth rather than higher inflation, equities should remain supported.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.