Market Recap – Week Ending March 1

Stocks Rally; Fed Policy Updates This Week

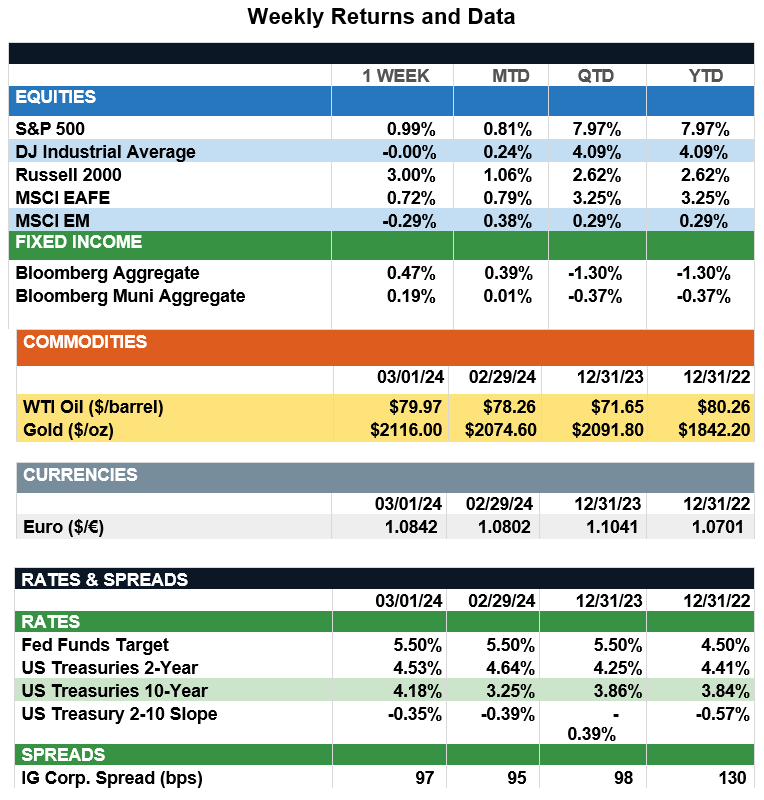

Overview: U.S. stocks continued to rally last week, as the S&P 500 index gained 1.0%. In addition, the tech-heavy Nasdaq index reached an all-time high on Friday, breaking the previous 2021 record. The S&P 500 index now has recorded gains in seven of the last eight weeks and is about 8.0% higher in total return year-to-date. Last week, inflation readings on both the headline and core PCE price index were in line with expectations, declining to 2.4% and 2.9%, respectively. Continued declining inflation, positive sentiment in artificial intelligence, and strong quarterly earnings have fueled recent market enthusiasm supporting stock returns. On the political front, Congress reached a deal last week that averted a government shutdown. Spending bills scheduled to expire last Friday were extended to March 8, and the bills scheduled to expire March 8 were extended for two additional weeks to March 22. Looking forward to this week, investors will look for clues about the future direction of interest rates as Federal Reserve Chair Jerome Powell provides policy updates to Congress on Wednesday and Thursday. Key economic data will come with the release of the nonfarm payrolls jobs report on Friday. Nonfarm payrolls are expected to increase 199,000 for February, with the unemployment rate to remain at 3.7%. Also of note will be average hourly earnings, which are expected to fall from 4.5% to 4.3% annualized. This wage inflation number is closely watched by the Fed as another indicator of the progress in bringing overall inflation down their long-term target of 2%.

Update on High-Yield Bonds (from JP Morgan): Given high short-term yields, many investors seeking income recently have piled into cash. Others, however, have been attracted to high-yield (HY) bonds, given yields of close to 8% in a falling inflation, steady growth environment. After two years of significant outflows, demand for HY has rebounded with January marking a third consecutive month of inflows. On the supply side, HY bond issuance also saw an uptick after hitting a decade low in 2022. However, demand pressures appear to be dominant, leading to a further 10bps compression of spreads year-to-date to 340bps. This spread reduction may also reflect a recent improvement in the quality of the HY index, with the bulk of bonds now rated BB and above. Moreover, near-term defaults should remain subdued as refinancing activity, which dominated the recent supply mix of HY bonds, has extended the maturities of most bonds well past 2027. That being said, some companies rated CCC or NR are facing refinancing challenges amidst stiff rates, leading to above-average defaults in that sector and dampening the overall recovery rate. While this may not translate to a broader surge in defaults, at least in the short run, investors should recognize spreads are priced for a perfect economic soft landing – they have only been tighter 5% of the time over the last quarter-century. Given the reinvestment risk of staying in cash, HY bonds present an attractive opportunity to lock in elevated yields. However, tight spreads and a wide dispersion in quality within the HY space point to the need for active management to achieve superior risk-adjusted returns.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.