Market Recap – Week Ending April 19

Stocks Lower Last Week; Key Earnings, Data This Week

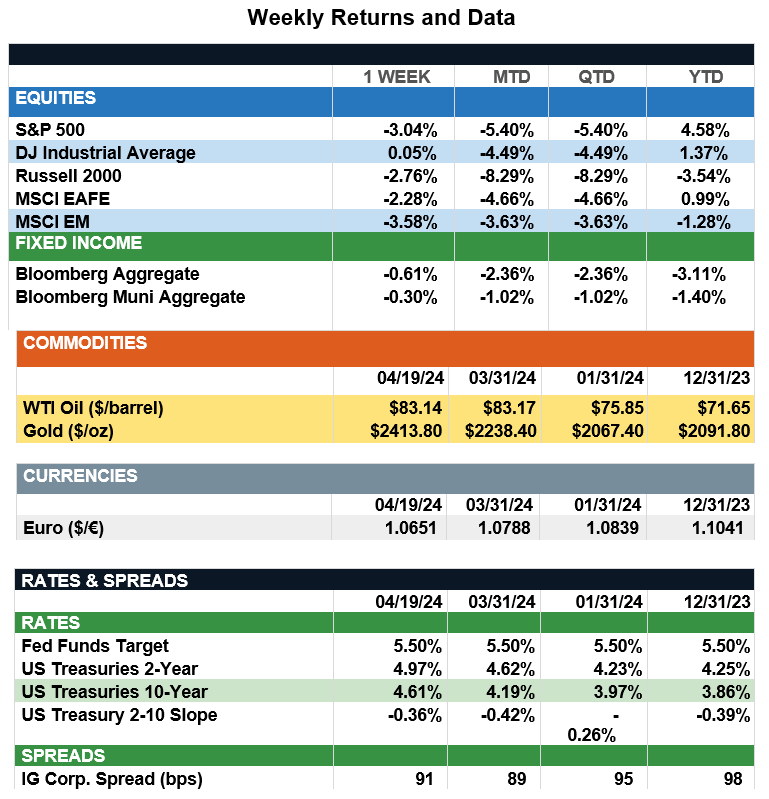

Overview: Stock across the globe were lower last week as interest rates increased with Federal Reserve Chair Jerome Powell saying rate cuts may come later than markets had been anticipating. In the U.S., the S&P 500 index had its worst week in more than a year, declining 3.0% for the week. In the bond markets, yields rose to the highest levels for the year with the 2-year and 10-Year U.S. Treasury notes finishing the week at yields of 4.97% and 4.61%, respectively. Looking ahead to this week, investors will be focused on key earnings reports from the likes of Microsoft, Meta, Tesla, Apple, Google, and Intel. On the economic data front, the first estimate of first-quarter gross domestic product (GDP) is due Thursday, with an expectation the economy grew at a 2.3% annualized pace for the period. A key inflation report will come on Friday in the form of the personal income and outlays report, which contains data on the personal consumption expenditure (PCE) price index, the Fed’s preferred measure of inflation. The core PCE Price index is expected to fall from 2.8% to 2.7% for the month of March on an annualized basis as the Fed continues to evaluate market data ahead of their next meeting, April 30-May 1.

Update on the Economy and Earnings (from JP Morgan): Recent economic data has continued to underscore the strength of the U.S. economy, and we anticipate GDP grew by 2.2% annualized during the first quarter. While this would be a deceleration relative to last quarter, above-trend growth should help prevent a meaningful slowdown in profit growth. With 72 companies having reported 1Q24 earnings, analysts are tracking pro-forma earnings per share (EPS) of $53.25. If realized, this would represent a y/y decline of 0.1% and a q/q decline of 4.1%. Of that annual change, revenues are expected to contribute 0.8% points, while margins and share buybacks are expected to subtract 0.6% points and 0.4% points, respectively. Based on reports so far and expected results, the growth sectors are largely expected to drive pro-forma earnings growth this quarter. Earnings in information technology and communication services are expected to grow 19.1% and 26.9% y/y, respectively. Within technology, strong demand for AI-related capabilities should continue to drive software earnings, while a rebound in PC shipments off suppressed levels could benefit the hardware segment. Consumer discretionary earnings are expected to grow 11.0% y/y, supported by resilient consumer demand, although a strong U.S. dollar and sluggish global economy will likely keep results in check. Elsewhere, financials are set to improve, while materials, industrials and health care are expected to see earnings contract, with materials and health care both tracking declines of over 20% y/y. Moreover, an average decline in natural gas prices of 24.8% y/y in the first quarter will likely hamper results in the energy sector. Overall, y/y earnings growth is expected to stay roughly flat with revenues, supported by strong economic activity, as the key driver. However, as economic momentum fades, margins will play an increasingly important role in maintaining profits.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC.

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.