Market Recap – Week ending June 16

Markets Have Strong Week After Fed Pauses Rate Hikes

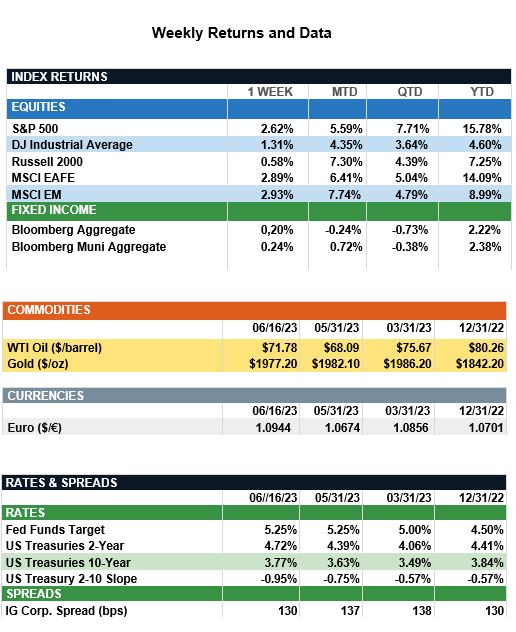

Overview: Stocks turned in a strong performance across the globe last week led by international (MSCI EAFE) and emerging markets (MSCI EM), both up 2.9% for the week. In the U.S., the S&P 500 reached a new year-to-date high and finished the week 2.6% higher in total return. Markets were buoyed by the Federal Reserve’s first pause in rates since their tightening cycle began 15 months ago. In their meeting last week, the Fed maintained the target fed funds rate at a range of 5.00-5.25%. However, two-thirds of the committee members projected two or more rate hikes this year, and the futures markets are currently pricing in about a 75% chance of an additional 25 basis point (0.25%) rate hike at the next Fed meeting in July. At his news conference following the conclusion of last week’s meeting, Fed Chair Jerome Powell highlighted a disappointingly slow decline in core inflation as a key reason for the revision to higher rate expectations. Meanwhile, Fed officials raised projections of gross domestic product (GDP) growth in 2023 from 0.6% to 1.0%, suggesting a continuation in positive growth in the economy for the balance of 2023. Economic data last week was encouraging, as U.S. headline inflation reached its lowest point since March 2021. Consumer prices (CPI) fell from 4.9% in April to 4.0% in May. Core prices showed a similar trend, with core CPI falling to 5.3% year-over-year. Consumer spending continues to show strength as well with retail sales rising 0.3% in May.

Update on Student Loan Debt (from JP Morgan): Last week, the Federal Reserve opted to keep the federal funds rate unchanged but hawkish messaging left the door open for further tightening in the coming months. In the Fed’s defense, economic growth so far has been resilient, suggesting the economy may be able to weather tighter conditions for longer. However, cracks are emerging, and one notable risk on the horizon is the resumption of student loan payments. The debt ceiling resolution bill mandated the pandemic student loan debt relief program end on June 30 as scheduled, with payments resuming in late August, regardless of an expected Supreme Court ruling on President Biden’s partial debt forgiveness program. In 1Q23, nearly 44 million Americans owed more than $1.6 trillion in federal student loan debt and, according to Moody’s, these borrowers will be faced with an average $250 monthly payment once payments resume. While this may not be a significant amount for many Americans, younger Americans hold the majority of student loan debt. This is notable because these consumers tend to have a higher marginal propensity to spend, greater credit card debt and smaller accumulated savings than their older counterparts, suggesting the payment resumption is likely to detract from spending in discretionary areas such as clothing and entertainment. Overall, we think the impact of forbearance ending should only be a moderate hit to the economy. However, it is coming at an inopportune time and even a modest consumer pullback will add to the economy’s vulnerability under the weight of monetary and credit tightening. With inflation falling and economic storm clouds gathering, the Fed may be too optimistic in believing that further tightening won’t put the economy into a significant recession, giving investors good reason for caution.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.