Market Recap – Week ending June 30

Stocks Higher; Encouraging Inflation Data

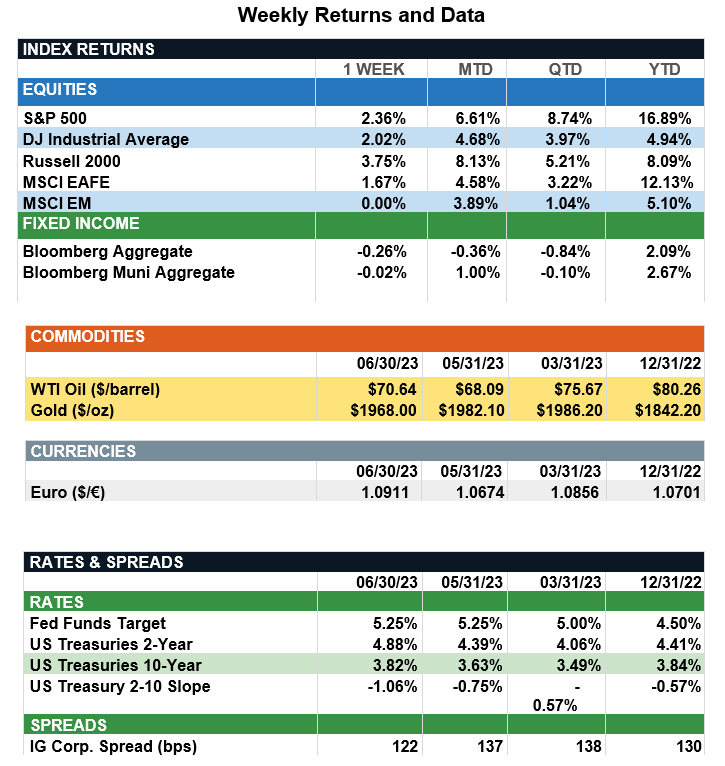

Overview: U.S. stocks closed the first half of 2023 in strong fashion last week with the S&P 500 index higher by 2.4%. Markets reacted positively to a strong durable goods report, an upward revision to second quarter GDP, and positive results from bank stress tests by the Federal Reserve. In addition, inflation data was encouraging, with the headline personal consumption (PCE Price Index) declining to 3.8% in June from 4.4% the previous month. Real Gross Domestic Product (GDP) growth was revised upward from 1.4% to 2.0%, driven by strong consumer spending and an increase in net trade. The Atlanta Fed’s GDPNow data now projects a growth rate of 2.2% for the second quarter of 2023, indicating continued positive economic growth. Consumer confidence has remained strong as the Conference Board index of consumer confidence increased to a level of 109.7 in June, above expectations. These robust numbers suggest the Federal Reserve may still have some work to do to rein in inflation, with futures markets now pricing in about an 85% chance of another 25-basis-point rate hike at the Fed meeting late this month.

Update on Market Performance (from JP Morgan): Stocks and bonds have had a strong start to the year due to resilient economic data, a bounce back in profit margins and a moderation in the market’s expectations for interest rates. That being said, while stocks and bonds have improved from their lows of 2022, commodities finished the first half of 2023 (1H23) down due to cooling energy prices and weakening global manufacturing demand. In terms of performance, U.S. large cap led the way, finishing 1H23 up 15.5%. However, despite the rally, returns have been entirely driven by the market’s largest stocks, with the top 10 companies in the S&P 500 accounting for more than 95% of the index’s YTD performance. Elsewhere, U.S. small caps lagged behind their large cap peers in 1H23 due to the lower quality of earnings and their greater exposure to cyclical sectors, which have underperformed this year. In the international markets, DM and EM increased 11.2% and 4.8%, respectively, in 1H23, as a weaker U.S. dollar and strong economic data in both regions buoyed returns. Some of this momentum, however, did wane toward the end of quarter in EM, as recent economic data from China have disappointed relative to expectations. Lastly, U.S. fixed income increased 1.8% in 1H23 due to a moderation in interest rates. Within the fixed income universe, global high yield performed well, as better than expected earnings have supported credit quality. While the default rate and downgrades-to-upgrades have increased, they both still remain below long-term averages. Looking ahead, investors should continue to be active and diversified, as the stock market’s narrow breadth, weakening expectations for forward earnings and the possibility of further rate hikes from the Fed could weigh on markets in the quarters ahead.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.