Market Recap – Week ending Aug. 18

Stock Lower; Strong Economic Data Raises Fed Concerns

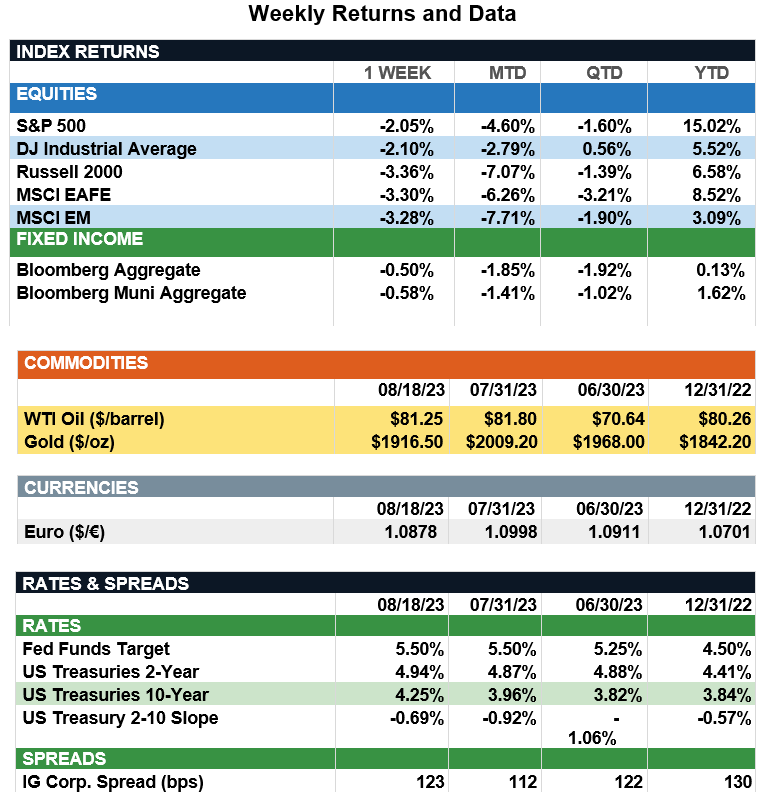

Overview: Stocks were lower across the globe last week following disappointing economic data in China and higher interest rates in the U.S. International developed stocks (MSCI EAFE) and emerging markets (MSCI EM) both finished the week 3.3% lower, while in the U.S. the S&P 500 index was down 2.1% on the week. Higher interest rates pressured bond returns with the broad-based taxable and municipal bond indices both finishing the week about 0.5% lower. The 2-year and 10-year Treasury yields rose, finishing the week at 4.94% and 4.25%, respectively. Strong economic data and growth trends have market participants concerned the Federal Reserve may still need to hike rates to tame inflation. The Atlanta Federal Reserve Bank GDPNow metric now predicts a 5.8% growth rate in third-quarter GDP, and data last week on retail sales, housing starts, and industrial production all were above expectations. The July FOMC meeting minutes noted most participants continue to see significant upside risks to inflation while acknowledging signs of easing price pressures. Investors will continue to watch for signals from the Fed as the balancing act between reducing inflation without tipping the economy into recession continues.

Update on Economic Growth (from JP Morgan): Most forecasters entered this year expecting a recession, but recently, economic growth has actually reaccelerated. In fact, the Atlanta Fed GDPNow model estimates the U.S. economy will grow at a 5.8% Saar this quarter. If realized, this would mark the fifth consecutive quarter of at or above-trend growth, highlighting the resiliency of this economy despite tighter monetary policy. The current estimate increased from 4.1% last week, driven by upside surprises on retail sales, housing starts and industrial production this week. Retail sales handily beat expectations, gaining 0.7% m/m and 1.0% ex-autos. While a 1.9% m/m increase in online sales contributed the most, gains were broad-based. Elsewhere, industrial production jumped by a stronger-than-expected 1.0% m/m due to strong auto production and sweltering temperatures driving up the demand for cooling. Manufacturing output also rose 0.5% m/m. However, excluding the sharp increase in motor vehicles and parts production, gains were a more modest 0.1%. Finally, the housing market showed continued signs of stabilization. Housing starts and permits rose by 3.9% and 0.1%, respectively, as gains in single-family more than offset declines in multi-family across both measures. Importantly, 5.8% growth is not guaranteed. Since 2Q 2014 and excluding the onset of COVID, the GDPNow model has overestimated the final GDP print by an average of 0.8% at this point in previous quarters, and by 2.2% when the model was above 4%. Still, strong economic momentum suggests the U.S. should avoid a recession in 2023 and has helped push yields higher. However, risks remain for 2024 and unless robust growth can be sustained, yields may be near their peak. With the 10-year at 15-year highs, investors can add to duration and lock in attractive income, leaving them better positioned for when yields inevitably move lower.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.