Market Recap – Week Ending Aug. 25

Stocks Positive; Powell Discusses Fed’s Intent

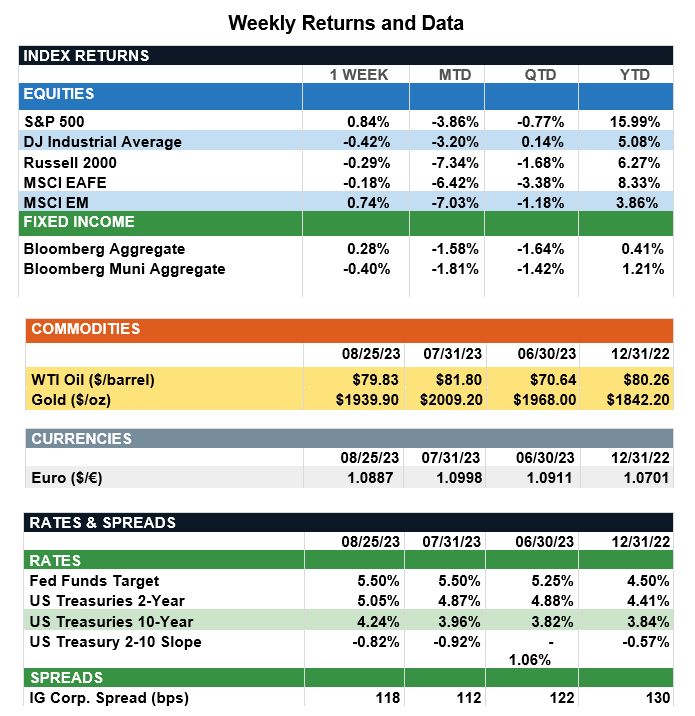

Overview: Stocks in the U.S. finished the week in positive territory last week, as the S&P 500 rose for the first time in four weeks and finished the week higher by 0.8%. Key news for the markets came on Friday from the economic symposium in Jackson Hole, Wyoming, where Federal Reserve Chair Jerome Powell summed up the intentions of the committee in his opening remarks: “It is the Fed's job to bring inflation down to our 2 percent goal, and we will do so. We have tightened policy significantly over the past year. Although inflation has moved down from its peak – a welcome development – It remains too high. We are prepared to raise rates further if appropriate and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.” Powell made it clear in his remarks the Fed is intent on continuing to progress toward their 2% inflation target, and yields rose last week on the news, with the 2-year Treasury finishing the week at a yield of 5.05%, its highest level in more than 15 years. As the Fed continues to evaluate economic data, key reports will come later this week. On Thursday, the Fed’s preferred measure of inflation, the core PCE Price Index, is expected to rise 4.2% on an annualized basis, up from 4.1% the prior month. The monthly employment report comes Friday, with a consensus of 170,000 new jobs and the unemployment rate expected to remain at 3.5%.

Update on Capital Spending (from JP Morgan): Earlier this year, investors largely anticipated U.S. economic activity, specifically capital spending, would slow due to the lagged impact of tighter monetary policy. Instead, however, the economy has remained resilient and real nonresidential fixed investment grew 4.6% y/y in 2Q, largely driven by spending on structures and intellectual property. Capital spending is being challenged by high vacancies in the office sector, softening manufacturing activity and the Hollywood writers’ strike. Nevertheless, the AI boom, recent fiscal policy incentives and solid demand for warehouses and green buildings remain areas of opportunity for intellectual property and structures investment. Capital spending appears to be entering a new era focused more on intellectual property spending, which is currently benefiting from the AI boom and also is less sensitive to interest rates than physical investment spending. Since 2020, this type of investment has been the largest percentage share of GDP for all nonresidential fixed investment components and currently accounts for 5.5% of GDP. Clearly, brains are becoming more favored relative to brawn when it comes to investment spending, so what does this mean for investors today? While last week’s August flash manufacturing. and services PMIs both showed a decline, and durable goods orders fell 5.2% in July, the economy still appears to have momentum. Provided businesses continue to boost investments in intellectual property, the economy should become less sensitive to rates, which, in turn, should benefit equity markets.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.