Market Recap – Week Ending Sept. 22

Stocks Continue Down Performance; PCE Price Index Due Friday

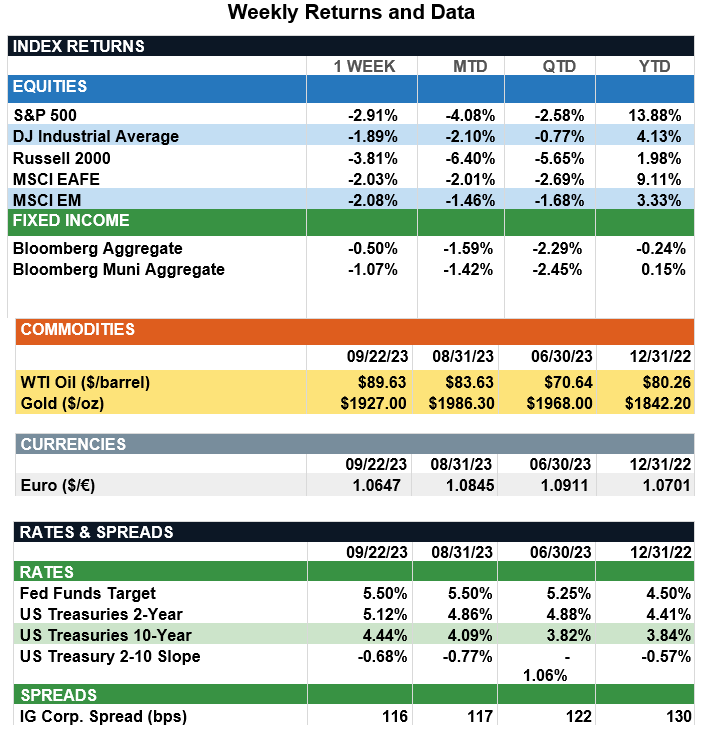

Overview: Stocks across the globe were lower last week, continuing the negative returns for September across all the major stock indices. In the U.S., the S&P 500 index was lower by 2.9% on the week and now is down about 4% for September. Focus in the markets now turns to concerns over a government shutdown, the prospect of interest rates “higher for longer” and the prospect of weaker consumer spending. With the House of Representatives failing to reach an agreement on a defense bill over the weekend and hardliners demanding spending cuts as part of any budget deal, odds are increasing the government may shut down Oct. 1. On the interest rate front, the 2-year and 10-year Treasury notes reached 15-year highs last week, finishing the week at 5.12% and 4.44%, respectively. At the Federal Open Market Committee (FOMC) meeting last week, the Fed left interest rates unchanged, yet projections now suggest the central bank members expect one additional 25 basis point rate hike by year-end. Market participants are not convinced of further rate hikes, however, as futures markets (CME Fedwatch) are showing only about a 40% chance of another increase in the funds rate by year-end. Data on inflation will be key to the decision with the Fed’s preferred measure of inflation, the PCE Price Index, due out Friday. Expectations are for the headline PCE to increase from 3.3% in July to 3.5% in August. Meanwhile, the Core PCE Price Index is projected to decline from 4.2% to 3.9% year-over-year.

Update on the Federal Reserve Outlook (from JP Morgan): Last week, the FOMC left policy rates unchanged at the current range of 5.25-5.50%. In its post-meeting statement, the FOMC maintained its hawkish bias, noting the “solid pace” of economic growth and that “inflation remains elevated.” Additionally, the FOMC’s dot plot showed the committee currently expects to hike once more before the end of the year and only cut by 50bps in 2024. Putting all this together, for markets, Wednesday’s FOMC meeting reiterated the “high for longer” narrative for interest rates and highlighted the importance of active management in the equity market. Higher interest rates typically correspond to an elevated level of equity return dispersion. Currently, S&P 500 return dispersion, on a LTM basis, is sitting at levels not seen since early 2010. At the sector level, energy stocks have had a strong quarter due to the uptick in oil prices and an emphasis on prioritizing shareholder returns over the last ~18 months. In contrast, while the tech-oriented sectors still are up year-to-date, performance has moderated on a quarter-to-date basis as the AI-driven rally has faded and higher interest rates weigh on valuations. Similarly, consumer discretionary has seen performance wane in 3Q, despite strong earnings results, as corporate guidance points toward a weakening outlook. Materials and industrials have struggled as well due to weakening manufacturing activity, while health care, utilities and real estate are currently all lagging the index due to elevated labor costs and higher rates. Looking ahead, we expect this divergence in performance within the S&P 500 to persist due to above-average inflation, elevated interest rates and an uncertain economic outlook. In such a scenario, investors should have a preference for low beta stocks with positive cash flows outside of capital-intensive industries.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg.

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.