Market Recap – Week Ending Sept. 8

Stocks Lower; CPI, Retail Sales Data This Week

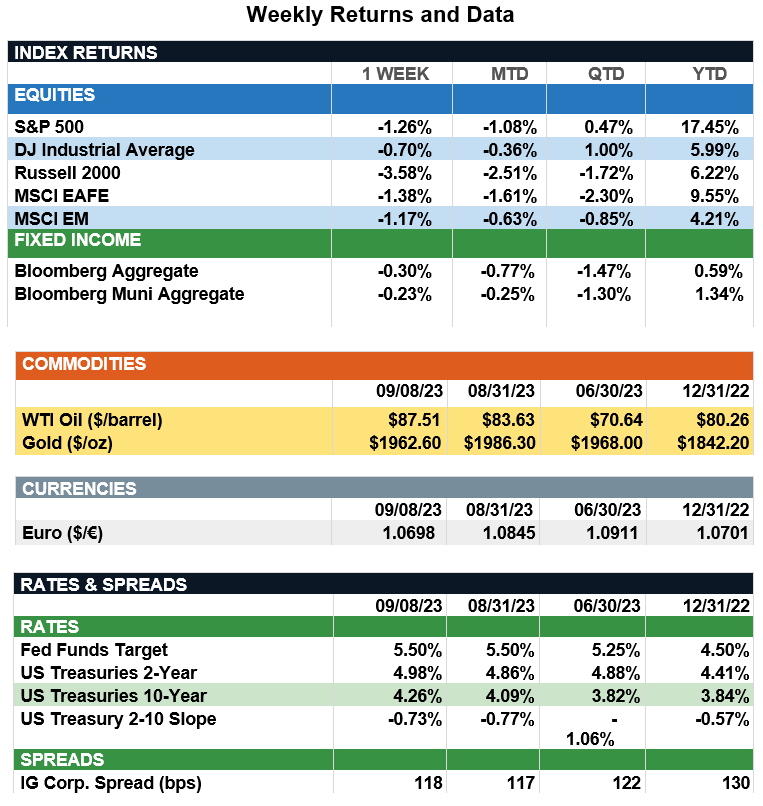

Overview: Stocks were lower across the globe last week with the S&P 500 index and international developed stocks (MSCI EAFE) both lower by about 1%. In the U.S., the S&P 500 index ended its two-week winning streak as market participants continued to search for direction. In bonds, higher interest rates weighed on bond prices with the yield on the 2-year and 10-year Treasury notes finishing the week around 5.0% and 4.30%, respectively. With earnings season in the rear-view mirror, monetary policy and interest rates are likely to remain the primary driver for both stocks in bonds in near-term. With the next Federal Reserve policy-setting meeting slated for Sept. 20, investors will keep a close eye on key inflation data later this week with the release of the Consumer Price Index (CPI) report on Wednesday. Economists are expecting headline inflation to increase by 3.6% on an annual basis, higher than last month’s reading of 3.2%. Higher gasoline prices are the likely culprit for the anticipated uptick in headline numbers, as oil prices have risen nearly 25% since the beginning of July. Nevertheless, we expect the markets and the Fed will be more interested in the Core CPI reading, which excludes the more volatile food and energy categories. Core prices are expected to have risen 4.3% on an annual basis, down from last month’s reading of 4.7%. In addition to inflation, retail sales data is expected on Thursday, which should provide some insight into the current state of the consumer. Assuming no major surprises on the data front this week, our expectations are for the Federal Reserve to hold off on further rate increases at the next meeting in September before potentially enacting one final rate hike in November.

Update on the Consumer (from JP Morgan): “Resilient” has been the word often associated with the U.S. economy in 2023, and much of this acclaim owes to strength in the U.S. consumer. In the second quarter, household consumption contributed over half of economic growth and is set to add a similar amount in the third quarter, according to the Atlanta Fed’s GDP nowcast. A tight labor market and rising real wages have provided support for consumers, but the ice may be thinner than consumption data alone suggest. By our measures, pandemic excess savings has dwindled to $0.2 trillion from its peak of $2.1 trillion, leading consumers to draw on revolving credit to finance their spending habits. Revolving credit as a share of disposable income may not look too worrying yet (at 6.3% in June compared to 6.5% pre-pandemic), but delinquencies for credit cards and auto loans are starting to rise. Flows into early delinquency status for credit cards rose to their highest level in 10 years in the second quarter and flows into serious delinquency (90+ days) are picking up as well. As such, the lags of monetary tightening may finally be weighing on consumer spending capacity, and with student loan payments restarting at the end of the month, summer’s shopping spree may be followed by a more pennywise back-to-school season. Indeed, consumer confidence in August dropped by nearly eight points to 106.1, reversing some of its gains in June and July. Investors seem to be heeding the same restraint as well, as skepticism over the potential for a soft landing and renewed upward pressures on energy prices contributed to lower stock prices last week. While the Fed may feel emboldened by a summer of economic resiliency, the clouds of recession have not departed just yet, and the best course of action likely remains one of both caution and patience.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.