Market Recap – Week Ending Oct. 20

Stocks Lower; GDP Estimate, Key Earnings This Week

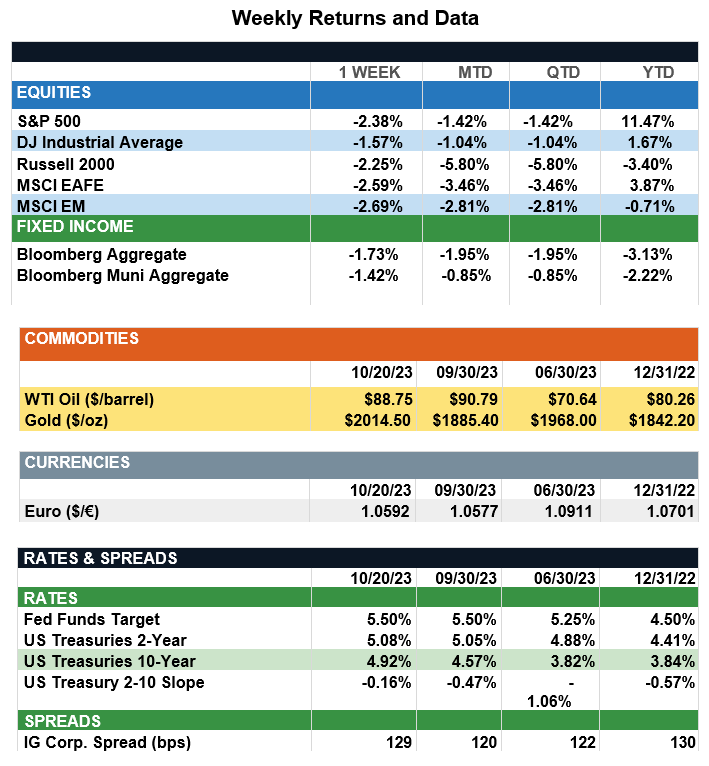

Overview: Stocks across the globe fell last week, with both U.S. and international stocks lower by more than 2% on the week. In the U.S., the S&P 500 index snapped a streak of three consecutive weeks of gains, ending the week 2.4% lower, as strong economic data has brought into question the end of the Federal Reserve’s rate hiking campaign. Fed Chair Jerome Powell’s comments last week that monetary policy could tighten further fueled a rise in interest rates, with the 10-year Treasury note increasing in yield from 4.57% to 4.92% on the week. Interest rates have continued to rise in recent weeks with the 10-year Treasury trading briefly above the 5% level in the latter part of the week, the highest level since July of 2007. Key events this week will be the release of the first estimate of third-quarter GDP growth and earnings highlighted by the technology sector. On the GDP front, growth is expected to be 4.1% for the quarter, with the robust economy adding to concerns the Fed may have to hike rates more to slow economic growth and continue to bring down inflation. On the earnings front, investors will look for key information for stock market direction from tech giants Amazon, Meta, and Microsoft, among others.

Update on the Consumer (from JP Morgan): Consumer strength has been one of the great surprises of 2023. Recent comprehensive GDP revisions suggest consumers still have a sizable excess savings cushion accumulated from government aid during the pandemic. Indeed, the Federal Reserve’s Distributional Financial Accounts report shows remarkable growth of 28% or $2.9tn in deposits in checking and savings accounts (including money market deposit accounts) between 4Q19 and 2Q23. Of course, households also have had to confront high inflation, so money put in the bank in 2020 isn’t worth the same today. On a real basis, the same measure of liquid assets is 9% higher than in 4Q19 – still decent growth, but well off its inflation-adjusted peak of 28%. The question then becomes, how are these savings distributed? The Fed report provides some insight. After adjusting for inflation, the bottom 80% have mostly exhausted their accumulation in cash deposits while the top 20% still retain a decent share of deposit growth. This support should allow for continued spending gains in areas such as luxury goods, leisure services and consumer durables, while challenging spending on consumer staples by lower and middle-income households. That being said, the economy counts by dollars and not heads, so even if strength is isolated to the top 20%, this can be a significant driver of economic growth. Overall, as strong retail sales data underscored last week, the consumer remains remarkably resilient, and savings cushions still look supportive even after the wave of pent-up spending last year.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.