Market Recap – Week Ending Oct. 27

Stocks Negative; Earnings, Employment Report This Week

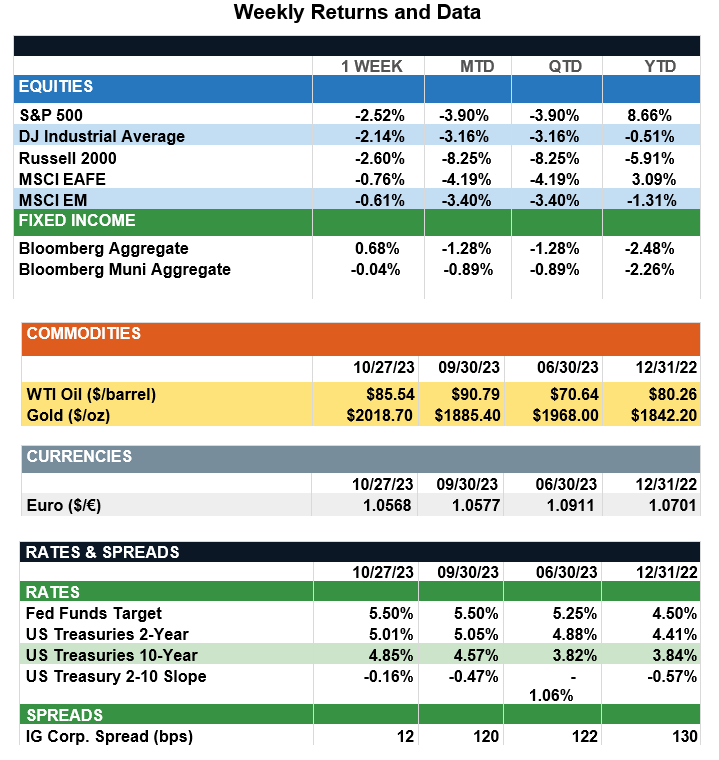

Overview: Stocks recorded negative performance across the globe last week, led in the U.S. by the S&P 500 index, which was down 2.5%. The broad-based S&P 500 now is down by 10.6% from its 2023 high and is off about 4% for the month-to-date in October, on pace for a third consecutive monthly decline. Investors continue to monitor economic data for clues to future Federal Reserve policy, as core personal consumption (Core PCE) declined to 3.7%, in line with expectations, while the initial estimate of gross domestic product (GDP) rose to 4.9% annualized in the third quarter. The strong GDP number has added to worries the Fed may need to raise rates further to slow the economy, yet futures data (CME FedWatch) predict a virtual certainty the Fed will keep the funds rate unchanged in the 5.25%-5.50% range at the conclusion of their two-day meeting this Wednesday, Nov. 1. In addition to the Fed meeting, the week will be highlighted by another busy earnings week (highlighted by Apple earnings Thursday), and the monthly employment report on Friday. October 2023 nonfarm payrolls are expected to increase by 183,000 (down from 336,000 in the prior month) with the unemployment rate projected to remain at 3.8%. An important part of the employment report will be average hourly earnings, which are expected to fall from 4.2% to 4.0% on a year-over-year basis. This “wage inflation” is closely monitored by the Fed and should provide insights as to the ongoing path of inflation.

Update on the Economy (from JP Morgan): Entering 2023, many analysts had penciled in a mild U.S. recession by mid-year. However, strong incoming economic data kept delaying the start date. Growth remained steady in the first half of the year, despite a hiccup in 1Q23 due to the regional banking crisis, and, more recently, a combination of positive impulses boosted 3Q23 GDP growth to a real annualized rate of 4.9% – the fastest pace in two years. Zooming in on specifics, a notable summer splurge, particularly by affluent households, propelled private consumption to 4% growth for the quarter. This surge contributed over half of the acceleration in real GDP growth. Inventory accumulation, typically a volatile component, was the second-largest contributor, as automakers stockpiled ahead of anticipated strikes. Housing shortages drove residential investment while national defense spending boosted the government’s contribution to GDP, each adding 0.2%-pts. On the flip side, non-residential investment was a major drag on growth, potentially indicating a cautious turn in business sentiment. While the headline GDP figure seems impressive at first sight, it likely overstates the strength of the economy. A recent backup in long-term yields has weighed on stocks and poses a risk to the spending surge by wealthier households through negative wealth effects. The positive impulses from inventory build-ups and government spending also will likely be transient; and while the Fed may acknowledge progress on core-PCE inflation when holding rates steady this week, it likely will keep the door open for a December rate hike. As a result, investors should brace for a slowing economy by maintaining well-balanced portfolios of financial assets and may want to consider adding alternatives that can provide durable streams of income, additional diversification, and more robust rates of return.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.